Estate Planning 2026: Federal Law Changes & Financial Impact on Your Legacy

As the calendar pages turn towards 2026, a significant shift is on the horizon for individuals and families engaged in estate planning. The federal tax landscape is poised for notable changes, particularly concerning the estate and gift tax exemptions, which could profoundly impact how wealth is transferred and legacies are preserved. Understanding these impending alterations is not merely a matter of compliance; it’s a critical step in proactively safeguarding your financial future and ensuring your wishes are honored.

Anúncios

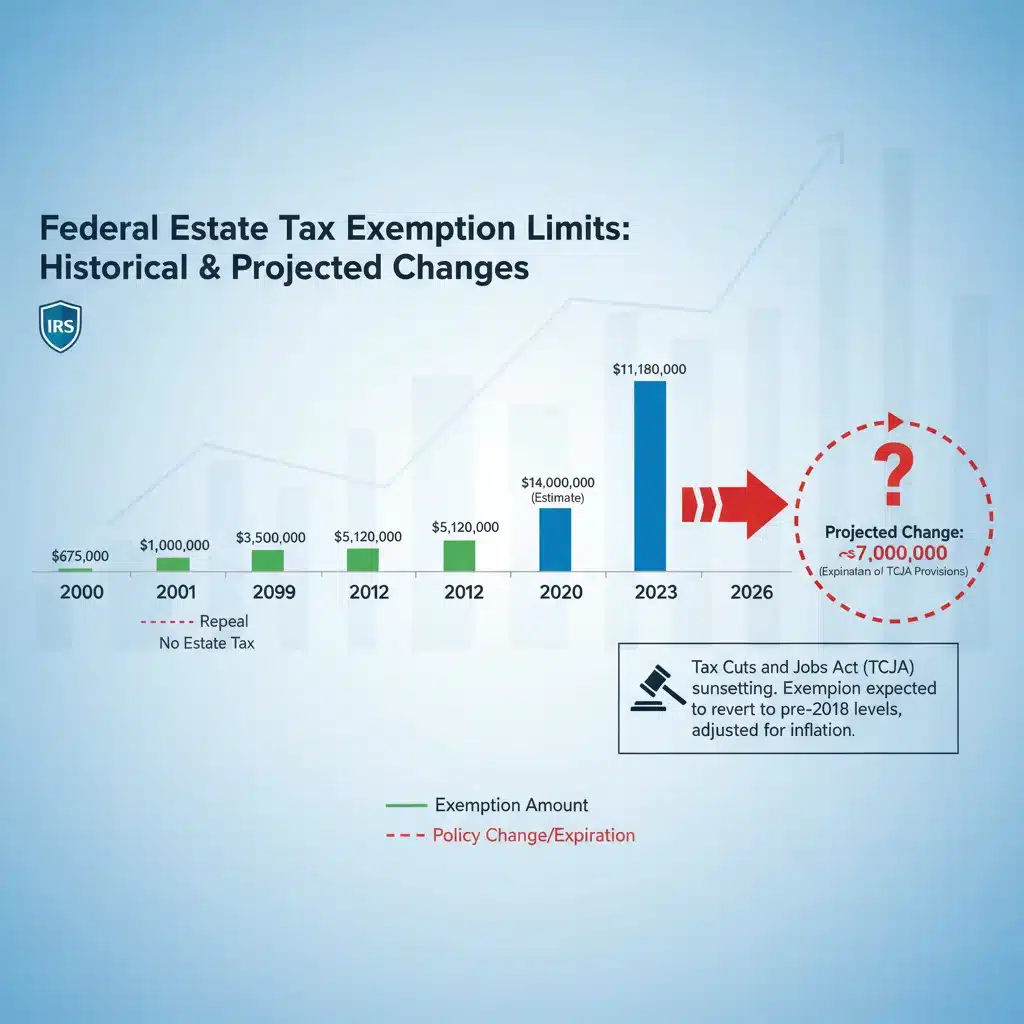

The Tax Cuts and Jobs Act (TCJA) of 2017 dramatically increased the federal estate and gift tax exemption amounts. However, many of these provisions are set to expire at the end of 2025, paving the way for a return to pre-TCJA levels, adjusted for inflation. This reversion will undoubtedly create a new set of challenges and opportunities for Estate Planning 2026. This comprehensive guide will delve into the specific federal law changes anticipated for 2026, explore their potential financial impact, and provide actionable strategies to help you navigate this evolving environment effectively.

Understanding the Impending Federal Law Changes for Estate Planning 2026

The cornerstone of the anticipated changes for Estate Planning 2026 lies in the expiration of key provisions from the TCJA. When the TCJA was enacted, it roughly doubled the federal estate, gift, and generation-skipping transfer (GST) tax exemptions. For 2023, this exemption stood at $12.92 million per individual, and for 2024, it rose to $13.61 million. Without new legislation, these amounts are scheduled to revert to approximately $6 million to $7 million per individual (adjusted for inflation from the 2011 baseline) starting January 1, 2026.

Anúncios

The Sunset of the TCJA’s Estate and Gift Tax Exemption Amounts

The most impactful change directly affecting Estate Planning 2026 is the scheduled ‘sunset’ of the increased federal estate and gift tax exemption. This means that, barring congressional action, the basic exclusion amount will be cut roughly in half. This reduction will subject a significantly larger number of estates to federal estate taxes than in recent years. For high-net-worth individuals, this could translate into substantial tax liabilities if their estate plans are not updated to reflect the new lower exemption.

It’s crucial to understand that the federal estate tax is levied on the fair market value of an individual’s assets at the time of their death, exceeding the exemption amount. The current top federal estate tax rate is 40%. A reduction in the exemption amount directly increases the taxable portion of an estate for those above the new threshold, leading to a potentially much higher tax bill.

Implications for the Generation-Skipping Transfer (GST) Tax Exemption

The GST tax exemption is intrinsically linked to the estate and gift tax exemption. It applies to transfers made to beneficiaries who are two or more generations younger than the donor (e.g., grandchildren). When the basic exclusion amount reverts in 2026, the GST tax exemption will also decrease proportionally. This change is particularly relevant for families aiming to establish multi-generational trusts or make significant gifts to grandchildren, as it will limit the amount that can be transferred free of GST tax. Strategic Estate Planning 2026 will need to consider how to optimize these transfers under the reduced exemption.

Portability of the Deceased Spousal Unused Exclusion (DSUE) Amount

The concept of portability, which allows a surviving spouse to use any unused portion of their deceased spouse’s federal estate tax exemption, will continue to be a vital tool. However, the amount that can be ported will also be subject to the reduced exemption. For example, if a spouse dies in 2025 with an unused exemption of $13.61 million, and the surviving spouse dies in 2026 or later, the amount they can port will be limited by the lower 2026 exemption. This nuance necessitates careful consideration in Estate Planning 2026 for married couples.

Financial Impact: Who Will Be Affected by Estate Planning 2026 Changes?

The impending changes will cast a wider net, impacting a broader spectrum of individuals and families. While the federal estate tax is often perceived as a concern only for the ultra-wealthy, the reduction in the exemption amount will bring many more affluent individuals into the fold of potential estate tax liability.

High-Net-Worth Individuals and Families

Clearly, high-net-worth individuals and families with significant assets will feel the most direct impact. Estates that were comfortably below the current $13.61 million exemption may suddenly find themselves facing federal estate tax exposure when the exemption drops to approximately $6 million to $7 million. This could lead to a substantial portion of their legacy being diverted to taxes rather than passing to their intended beneficiaries. Proactive Estate Planning 2026 becomes paramount for this group.

Business Owners and Inherited Family Businesses

For owners of successful family businesses, the impact can be particularly acute. A significant portion of their wealth is often tied up in illiquid assets, such as the business itself. If the estate faces a large tax bill, beneficiaries might be forced to sell off parts of the business or even the entire enterprise to cover the estate taxes, potentially jeopardizing the family legacy and the continuity of the business. This makes specialized Estate Planning 2026 strategies for business succession critical.

Individuals with Large Real Estate Holdings

Those with substantial real estate portfolios, especially in appreciating markets, may also find their estates exceeding the reduced exemption. Unlike liquid assets, real estate can be difficult to divide or sell quickly without incurring significant costs or losing value. This can create liquidity issues for the estate and its inheritors, emphasizing the need for advanced planning in Estate Planning 2026.

Married Couples and Joint Estates

While portability offers a mechanism for married couples to combine their exemptions, the overall reduction still means a smaller combined exclusion. Couples with a combined net worth exceeding the new, lower exemption (e.g., $12 million to $14 million) will need to re-evaluate their joint estate plans to minimize tax exposure and ensure efficient wealth transfer. Strategic use of trusts and other tools within Estate Planning 2026 will be essential.

Proactive Strategies for Estate Planning 2026

Given the impending changes, waiting until 2026 is not advisable. Proactive planning can help mitigate the financial impact and ensure your estate plan remains robust and aligned with your goals. Here are several key strategies to consider for Estate Planning 2026:

1. Maximize Gifting Before the Exemption Sunset

One of the most effective strategies for Estate Planning 2026 is to utilize the current higher gift tax exemption before it reverts. You can make substantial gifts to beneficiaries now, effectively removing those assets from your taxable estate. The IRS has confirmed that gifts made under the higher exemption amounts will not be clawed back or taxed later, even if the exemption decreases. This ‘use it or lose it’ opportunity is significant.

- Direct Gifts: Consider making large direct gifts to children, grandchildren, or other beneficiaries.

- Irrevocable Trusts: Establish irrevocable trusts (e.g., Crummey trusts, Spousal Lifetime Access Trusts (SLATs)) and fund them with assets up to the current exemption amount. These trusts can remove assets from your estate while potentially providing for beneficiaries.

- Annual Exclusion Gifts: Remember that the annual gift tax exclusion (currently $18,000 per donee in 2024) is separate from the lifetime exemption and can be used each year without impacting your lifetime exclusion.

2. Review and Update Existing Estate Documents

Your current will, trusts, and other estate planning documents may have been drafted under different tax laws. It’s imperative to review them with an estate planning attorney to ensure they still achieve your objectives in light of the Estate Planning 2026 changes.

- Wills: Ensure your will reflects your current wishes for asset distribution and guardian appointments.

- Trusts: Re-evaluate existing trusts, especially those designed for tax efficiency, to confirm they remain effective under the new exemption levels. Consider establishing new trusts if appropriate.

- Beneficiary Designations: Check beneficiary designations on life insurance policies, retirement accounts (IRAs, 401(k)s), and annuities. These supersede your will and are critical for proper asset transfer.

3. Consider Advanced Wealth Transfer Strategies

For those with very large estates, more sophisticated strategies might be necessary for proactive Estate Planning 2026.

- Grantor Retained Annuity Trusts (GRATs): A GRAT allows you to transfer appreciating assets out of your estate with minimal gift tax consequences, especially in a low-interest-rate environment.

- Charitable Lead Trusts (CLTs) and Charitable Remainder Trusts (CRTs): These trusts can provide significant tax benefits while fulfilling philanthropic goals. They can reduce your taxable estate and potentially provide income streams.

- Intentionally Defective Grantor Trusts (IDGTs): IDGTs can be used to freeze the value of appreciating assets for estate tax purposes, allowing future appreciation to pass to beneficiaries free of estate tax.

- Family Limited Partnerships (FLPs) and Limited Liability Companies (LLCs): These entities can be used to hold and transfer assets, potentially allowing for valuation discounts for gift and estate tax purposes.

4. Reassess Business Succession Plans

Business owners should critically re-evaluate their succession plans. The reduced exemption might necessitate different strategies for transferring business ownership to the next generation or to key employees without triggering excessive estate taxes. This could involve buy-sell agreements, recapitalization, or gifting strategies tailored for business interests as part of Estate Planning 2026.

5. Review Life Insurance Needs

Life insurance can be a powerful tool in Estate Planning 2026, especially for providing liquidity to an estate to cover potential estate tax liabilities without forcing the sale of illiquid assets like a family business or real estate. Consider placing life insurance policies in an Irrevocable Life Insurance Trust (ILIT) to keep the death benefit out of your taxable estate.

6. Optimize for State Estate Taxes

Remember that federal estate tax is only one piece of the puzzle. Many states also impose their own estate or inheritance taxes, often with much lower exemption thresholds than the federal government. The federal changes in Estate Planning 2026 will not directly alter state laws, but it’s an opportune time to review your state’s specific requirements and integrate them into your overall plan.

The Role of Professional Advice in Estate Planning 2026

Navigating the complexities of federal tax law and its impact on your estate requires specialized knowledge. Attempting to manage these changes without professional guidance can lead to costly errors and missed opportunities. Engaging a team of experienced professionals is crucial for effective Estate Planning 2026.

Estate Planning Attorneys

An estate planning attorney is essential for drafting and updating legal documents, ensuring they comply with current and future laws, and accurately reflect your intentions. They can advise on the most suitable trusts, wills, and other legal instruments to achieve your goals while minimizing tax exposure.

Financial Advisors

A financial advisor can help you understand the current value of your assets, project future growth, and assess the potential impact of tax law changes on your overall financial picture. They can work with your attorney to integrate your investment strategy with your estate plan, ensuring your assets are positioned effectively for transfer.

Tax Professionals (CPAs)

A Certified Public Accountant (CPA) specializing in estate and gift tax can provide critical insights into the tax implications of various strategies. They can help calculate potential tax liabilities, explore deductions, and ensure all filings are correct and timely.

Beyond Taxes: Holistic Estate Planning 2026

While tax implications are a significant driver for Estate Planning 2026, remember that estate planning encompasses much more than just minimizing taxes. It’s about ensuring your legacy, securing your loved ones’ future, and articulating your wishes for healthcare and financial management should you become incapacitated.

Healthcare Directives and Powers of Attorney

These documents are critical regardless of your net worth. A healthcare directive (or living will) specifies your wishes for medical treatment, while a durable power of attorney for healthcare designates someone to make medical decisions on your behalf. A durable financial power of attorney grants someone the authority to manage your financial affairs if you are unable to do so.

Guardianship for Minor Children

If you have minor children, your estate plan should clearly designate guardians. This ensures that in the event of your passing, your children will be cared for by individuals you trust, avoiding potential court battles and ensuring their well-being.

Digital Assets

In our increasingly digital world, don’t overlook your digital assets. This includes online accounts, social media profiles, digital photos, and cryptocurrencies. Your estate plan should address how these assets are managed and transferred, and who has access to them.

The Economic and Political Landscape Influencing Estate Planning 2026

It’s important to acknowledge that the future of Estate Planning 2026 is not set in stone. While the TCJA provisions are scheduled to sunset, Congress could intervene with new legislation before the end of 2025. The political climate and the outcome of upcoming elections could significantly influence whether the current exemption levels are extended, modified, or allowed to revert as planned.

Therefore, estate planning must remain flexible and adaptive. Staying informed about legislative developments and working closely with your advisors will be key to making timely adjustments to your plan. This dynamic environment underscores the importance of not just having an estate plan, but having a living, evolving plan that can adapt to changing laws and personal circumstances.

Case Study: The Proactive Approach to Estate Planning 2026

Consider the case of the Chen family. Mr. and Mrs. Chen, both successful entrepreneurs, have a combined estate valued at approximately $20 million, primarily in their business and real estate holdings. They have three adult children and several grandchildren. Under the current 2024 exemption of $13.61 million per person, their estate would likely pass to their children with minimal federal estate tax liability.

However, recognizing the impending changes for Estate Planning 2026, they met with their estate planning team in late 2024. Their attorney advised them to utilize the current higher exemption. They decided to establish two Spousal Lifetime Access Trusts (SLATs), one for each spouse, and funded them with a total of $18 million in appreciating assets from their business interests. These trusts were structured to benefit their children and grandchildren, while still providing limited access for the spouse who didn’t establish the trust, if needed.

By making these significant gifts before the end of 2025, the Chens effectively removed $18 million from their taxable estate. Even if the exemption reverts to $6 million per person in 2026, their remaining estate would be well within the new combined exemption amount, significantly reducing their potential federal estate tax exposure. This proactive Estate Planning 2026 move allowed them to secure their legacy and minimize future tax burdens for their heirs.

Conclusion: Secure Your Legacy with Strategic Estate Planning 2026

The year 2026 marks a pivotal moment for estate planning in the United States. The scheduled reversion of the federal estate and gift tax exemptions will necessitate a careful re-evaluation of existing plans and the implementation of new strategies. While the precise details of future legislation may evolve, the prudent course of action is to plan based on the current sunset provisions.

Don’t wait for 2026 to arrive. Engage with qualified estate planning attorneys, financial advisors, and tax professionals now. By understanding the potential impact of these federal law changes and taking proactive steps to update your estate plan, you can protect your assets, minimize tax liabilities, and ensure your legacy is preserved according to your wishes. Estate Planning 2026 is not just about reacting to changes; it’s about strategically shaping your financial future and the future of those you care about most.

Frequently Asked Questions About Estate Planning 2026

- What is estate planning?

- Estate planning is the process of arranging for the management and disposal of your estate during your life and after your death. It involves creating legal documents such as wills, trusts, powers of attorney, and healthcare directives to ensure your assets are distributed according to your wishes, minimize taxes, and provide for your loved ones.

- What are the main federal law changes expected for Estate Planning 2026?

- The primary change expected for Estate Planning 2026 is the ‘sunset’ of the increased federal estate, gift, and generation-skipping transfer (GST) tax exemptions from the Tax Cuts and Jobs Act of 2017. This means the exemption amounts are expected to revert to approximately $6 million to $7 million per individual (adjusted for inflation) from their current levels of over $13 million.

- How will the reduced exemption affect my estate?

- If your net worth (including all assets like real estate, investments, and business interests) exceeds the new, lower exemption amount, a portion of your estate will be subject to federal estate tax (currently at a top rate of 40%). This could significantly reduce the amount of wealth passed to your beneficiaries.

- What is the ‘use it or lose it’ opportunity?

- The ‘use it or lose it’ opportunity refers to the ability to make substantial gifts up to the current, higher federal gift tax exemption amount before it is scheduled to revert at the end of 2025. The IRS has confirmed that these gifts will not be clawed back or re-taxed even if the exemption decreases later.

- Should I update my will and trusts because of Estate Planning 2026?

- Absolutely. It is highly recommended to review and update all your estate planning documents, including wills and trusts, with an estate planning attorney. Your current documents may not be optimized for the new tax environment, and changes may be needed to ensure your legacy is protected and your wishes are fulfilled.

- What is portability, and how does it relate to Estate Planning 2026?

- Portability allows a surviving spouse to use any unused portion of their deceased spouse’s federal estate tax exemption. While portability will continue, the amount that can be ported will be based on the lower exemption amount in effect at the time of the surviving spouse’s death or when the portability election is made, impacting the overall combined exclusion for married couples.

- Do state estate taxes also change in 2026?

- The federal law changes for Estate Planning 2026 do not directly alter state estate or inheritance tax laws. However, it’s a good time to review your state’s specific tax regulations, as many states have their own, often lower, exemption thresholds that could also impact your estate.

- When should I start planning for these changes?

- The time to start planning is now. Given that the changes are scheduled for January 1, 2026, taking action in 2024 and 2025 allows you to capitalize on the current higher exemptions and strategically prepare your estate for the future. Procrastination could lead to missed opportunities and increased tax liabilities.