Decoding the 3-Month Dip: U.S. Consumer Confidence Explained

Anúncios

The economic landscape is a complex tapestry woven from various threads, and one of the most crucial is consumer confidence. It’s a barometer of how optimistic or pessimistic consumers feel about their financial prospects and the overall economy. When consumer confidence is high, people are more likely to spend, invest, and drive economic growth. Conversely, a dip in this sentiment often signals caution, reduced spending, and potential economic headwinds. Recently, the United States has witnessed a notable three-month dip in consumer confidence, a trend that has economists, policymakers, and everyday citizens alike asking, ‘What’s going on?’

Anúncios

Understanding this consumer confidence dip isn’t just an academic exercise; it has real-world implications for everything from retail sales and housing markets to employment figures and investment strategies. This comprehensive analysis will delve into the various factors contributing to this downturn, explore its potential consequences, and offer insights into what the future might hold. We’ll examine key economic indicators, the persistent shadow of inflation, labor market dynamics, and the psychological impact of global and domestic events on the American consumer.

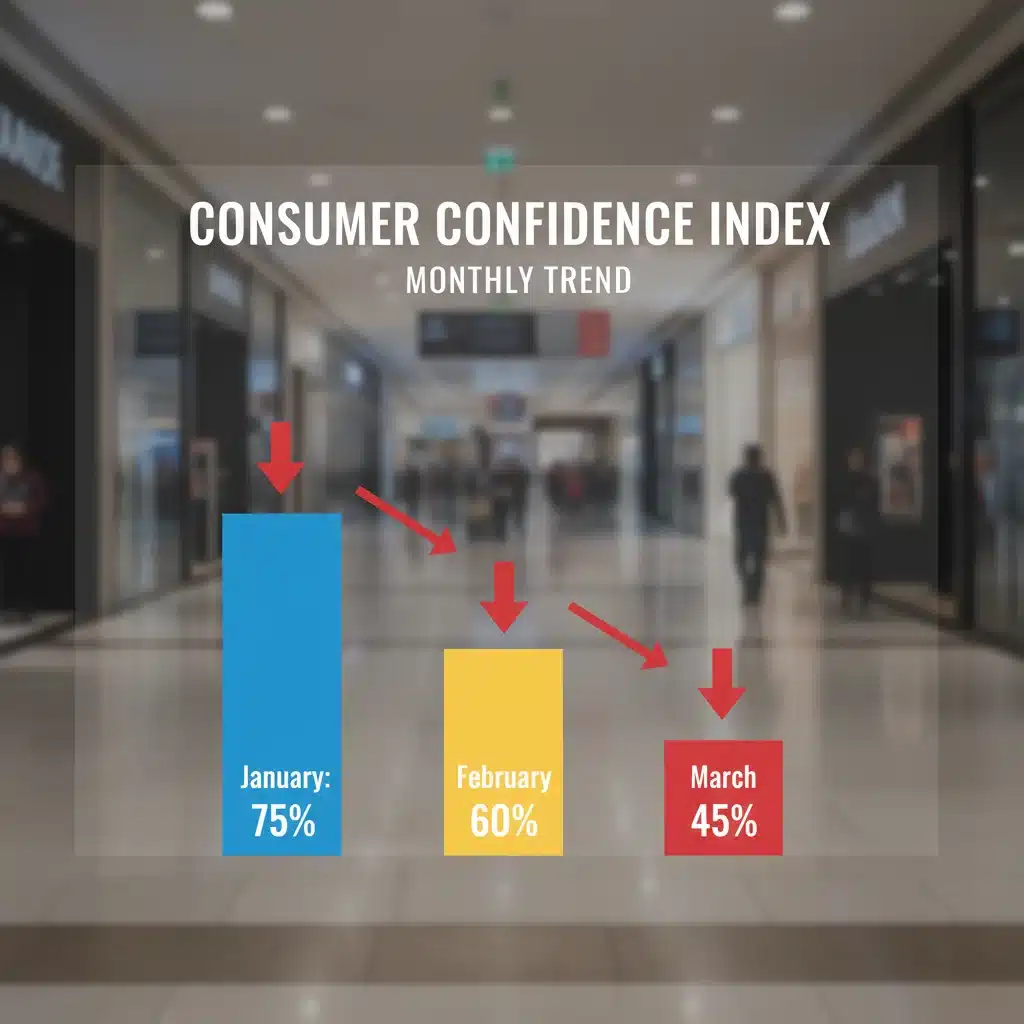

The concept of consumer confidence is typically measured by surveys that gauge consumers’ perceptions of current economic conditions and their expectations for the future. Organizations like The Conference Board and the University of Michigan conduct these surveys, asking questions about job prospects, business conditions, and personal financial situations. A sustained decline, such as the recent three-month dip, suggests a shift in collective sentiment that warrants close attention.

Anúncios

Understanding the Metrics: How Consumer Confidence is Measured

Before we dissect the reasons behind the recent consumer confidence dip, it’s essential to understand how this vital economic indicator is measured. Two primary surveys in the U.S. provide crucial insights: The Conference Board Consumer Confidence Index and the University of Michigan Consumer Sentiment Index.

The Conference Board Consumer Confidence Index

This index is derived from a monthly survey of 5,000 U.S. households. It consists of two sub-indices:

- Present Situation Index: Reflects consumers’ assessment of current business and labor market conditions.

- Expectations Index: Captures consumers’ short-term outlook (next six months) regarding income, business, and labor market conditions.

The questions cover various aspects, such as ‘How would you rate present business conditions?’ and ‘What do you think the situation will be like six months from now regarding business conditions?’ The responses are compiled, weighted, and then indexed to a base year (currently 1985=100).

University of Michigan Consumer Sentiment Index

Similar to The Conference Board’s survey, the University of Michigan’s index also measures consumer attitudes and expectations. It’s based on telephone interviews with 500 households each month. This survey also has components focusing on current conditions and future expectations, particularly gauging consumers’ feelings about their personal finances and the economy’s short- and long-term prospects.

Both indices provide valuable, though sometimes slightly differing, perspectives on consumer sentiment. A consistent decline across both, as has been observed recently, offers a strong signal about the prevailing mood of American consumers. The three-month dip we are analyzing indicates that this sentiment isn’t just a fleeting blip but a more entrenched trend.

Key Drivers Behind the Recent Consumer Confidence Dip

Several interconnected factors are likely contributing to the observed consumer confidence dip. Pinpointing the exact weight of each can be challenging, but a holistic view reveals a confluence of economic pressures and uncertainties.

Persistent Inflation and Cost of Living

Perhaps the most significant factor impacting consumer sentiment is the persistent high inflation. For over a year, Americans have grappled with elevated prices for everyday necessities: groceries, fuel, housing, and utilities. While inflation rates have shown signs of cooling from their peaks, they remain well above the Federal Reserve’s target of 2%. This means that even if prices aren’t rising as rapidly, they are still significantly higher than they were a couple of years ago, eroding purchasing power and making household budgets tighter.

When consumers see their paychecks buy less, their financial outlook darkens. The feeling of ‘running in place’ or even ‘falling behind’ despite working hard can severely dampen optimism. The constant need to make difficult choices between essentials or cut back on discretionary spending weighs heavily on the mind of the average consumer. This sustained pressure on household finances is a direct contributor to the consumer confidence dip.

Interest Rate Hikes and Borrowing Costs

In response to inflation, the Federal Reserve has aggressively raised interest rates. While necessary to cool down an overheating economy, these rate hikes have a direct impact on consumers. Borrowing money for major purchases like homes, cars, or even using credit cards has become significantly more expensive. This increased cost of borrowing can deter consumers from making big-ticket purchases, which are often indicators of strong economic confidence.

The housing market, in particular, has felt the pinch. Higher mortgage rates have priced many potential homebuyers out of the market or significantly reduced their purchasing power. Similarly, businesses facing higher borrowing costs may scale back expansion plans, which can indirectly affect job growth and wage increases, further impacting consumer sentiment.

Labor Market Dynamics and Job Security Concerns

While the U.S. labor market has remained relatively robust, with low unemployment rates, there are nuances that could be contributing to the consumer confidence dip. Anecdotal evidence and some data points suggest a cooling in certain sectors, with a few high-profile layoffs making headlines. Even if overall unemployment remains low, concerns about job security can quickly spread, especially if individuals perceive their industry or company as vulnerable.

Wage growth, while present, has struggled to keep pace with inflation for many workers, meaning their real wages (purchasing power) have declined. This disconnect can lead to feelings of economic insecurity, even for those who are employed. The fear of a potential recession, often accompanied by job losses, also looms large, influencing consumers’ willingness to spend and their overall financial outlook.

Geopolitical Instability and Global Economic Slowdown

Beyond domestic economic factors, global events cast a long shadow. Ongoing geopolitical conflicts, such as the war in Ukraine, continue to fuel uncertainty in energy markets and supply chains. The slowdown in major global economies, like China and parts of Europe, also raises concerns about export demand for U.S. goods and services, potentially impacting corporate profits and investment.

These external factors, while sometimes feeling distant, contribute to a general sense of unease. Consumers are aware that global instability can have ripple effects, influencing everything from gas prices to the availability of imported goods. This broad uncertainty can make individuals more cautious about their financial decisions, contributing to the overall consumer confidence dip.

Stock Market Volatility and Wealth Effect

For many Americans, their wealth is tied to the stock market through retirement accounts, investments, and other holdings. Periods of stock market volatility, even if temporary, can make consumers feel less wealthy and more cautious. The ‘wealth effect’ suggests that when people feel richer, they spend more; conversely, when their investment portfolios shrink, they tend to cut back.

Recent fluctuations and corrections in the stock market, coupled with the general economic uncertainty, can lead consumers to pull back on discretionary spending and save more, further contributing to the decline in confidence.

The Ramifications of a Sustained Consumer Confidence Dip

A sustained consumer confidence dip is not merely a statistical anomaly; it has tangible consequences for various sectors of the economy and for individual households.

Impact on Consumer Spending

The most direct impact of declining consumer confidence is on spending. When consumers are pessimistic about the future, they tend to reduce discretionary purchases, save more, and focus on essential goods and services. This slowdown in spending can ripple through the economy, affecting:

- Retail Sales: Non-essential retail categories, from electronics to apparel, often see a decline in sales.

- Automotive Industry: Big-ticket items like new cars become less attractive when consumers are uncertain about their job security or future income.

- Travel and Leisure: Vacations, dining out, and entertainment are often among the first areas where consumers cut back.

A significant reduction in consumer spending can lead to slower economic growth, as consumer expenditure accounts for a substantial portion of the U.S. GDP.

Business Investment and Hiring

Businesses closely watch consumer confidence as an indicator of future demand. If consumers are pulling back, businesses may become hesitant to invest in new projects, expand operations, or hire new employees. This cautious approach can lead to a self-fulfilling prophecy: reduced business investment can slow job creation, which further dampens consumer confidence.

Small businesses, which are often more sensitive to changes in consumer demand, can be particularly vulnerable during periods of low confidence. Their ability to weather a slowdown in sales might be limited, potentially leading to layoffs or even closures.

Housing Market Dynamics

The housing market is highly sensitive to consumer sentiment and interest rates. A consumer confidence dip, especially when coupled with high mortgage rates, can significantly cool down housing activity. Potential homebuyers may postpone their purchases, leading to fewer sales and potentially softer price growth, or even declines in some areas.

Current homeowners might also feel the pinch if they were considering selling, as a less robust market could mean lower offers or longer selling times. The psychological impact of a perceived decline in home values can further contribute to a general sense of economic anxiety.

Policy Implications and Federal Reserve Response

Policymakers, particularly the Federal Reserve, pay close attention to consumer confidence. A sustained dip can signal that their efforts to curb inflation might be having a broader impact than intended, potentially pushing the economy towards a recession. This could influence future monetary policy decisions, such as the pace of interest rate hikes or even discussions about potential rate cuts if economic conditions deteriorate significantly.

Government fiscal policy might also be affected. Lawmakers might consider stimulus measures or other interventions to boost consumer spending and confidence if the economic outlook becomes too bleak. However, such decisions are often complex, balancing the need for economic support with concerns about inflation and national debt.

Looking Ahead: Navigating the Uncertainty

The recent three-month consumer confidence dip serves as a crucial signal for the U.S. economy. While it doesn’t automatically mean a recession is imminent, it does suggest that consumers are feeling the pinch and are becoming more cautious. Navigating this period of uncertainty requires a nuanced understanding of the underlying factors and a proactive approach from both individuals and institutions.

For Consumers: Prudence and Preparedness

For individual consumers, a period of declining confidence often calls for financial prudence. This might include:

- Budgeting and Expense Review: Carefully tracking income and expenses to identify areas for savings.

- Building Emergency Savings: Strengthening financial safety nets to weather unexpected job losses or economic downturns.

- Debt Management: Prioritizing paying down high-interest debt, especially with rising interest rates.

- Cautious Spending: Delaying non-essential large purchases and re-evaluating discretionary spending.

While it’s important not to panic, being prepared for potential economic headwinds can provide a sense of security and resilience.

For Businesses: Adaptability and Strategic Planning

Businesses need to be agile and responsive to shifts in consumer sentiment. This could involve:

- Re-evaluating Marketing Strategies: Focusing on value and essential needs rather than luxury or discretionary items.

- Optimizing Operations: Looking for efficiencies to manage costs in a potentially slower demand environment.

- Workforce Planning: Strategically managing hiring and retention to align with anticipated demand.

- Diversifying Revenue Streams: Exploring new markets or product offerings that might be less sensitive to economic downturns.

Understanding that consumers are more cautious can help businesses tailor their offerings and communications to better meet evolving needs.

For Policymakers: Balancing Act and Clear Communication

Policymakers face the delicate task of balancing inflation control with economic stability. The Federal Reserve will likely continue to monitor a wide array of economic data, including consumer confidence, as it makes decisions on interest rates. Clear and consistent communication from economic authorities is crucial to manage expectations and prevent unnecessary panic.

Government initiatives that support job creation, provide targeted relief, or invest in long-term economic growth can also play a role in shoring up consumer confidence during challenging times. The challenge lies in implementing such policies without exacerbating inflationary pressures.

Historical Context: Previous Dips and Recoveries

It’s important to put the current consumer confidence dip into historical context. The U.S. economy has experienced numerous periods of declining consumer sentiment, often preceding or coinciding with economic slowdowns or recessions. However, it’s also important to remember that consumer confidence is not a perfect predictor and can sometimes rebound quickly.

For instance, significant dips were observed during the dot-com bubble burst in the early 2000s, the 2008 financial crisis, and the initial stages of the COVID-19 pandemic. Each period had its unique set of drivers and economic consequences. The recovery from these dips often depended on the resolution of the underlying issues – whether it was a return to job growth, stabilization of financial markets, or the containment of a public health crisis.

The current situation is unique due to the combination of persistent inflation, aggressive interest rate hikes, and lingering geopolitical uncertainties. However, understanding how the economy has navigated similar challenges in the past can offer valuable lessons and perspectives on potential paths to recovery.

The Psychological Aspect: Fear vs. Reality

Beyond the hard economic data, consumer confidence is deeply rooted in psychology. Perceptions, expectations, and even media narratives can significantly influence how people feel about their financial future. The fear of a recession, even if not fully materialized, can become a self-fulfilling prophecy if it leads to widespread cutbacks in spending and investment.

Conversely, positive news, such as a significant drop in inflation, strong job numbers, or a resolution to global conflicts, can quickly turn the tide of sentiment. The challenge for policymakers and economic leaders is to manage these psychological factors, providing clear information and fostering an environment where optimism can grow organically.

The three-month consumer confidence dip is a clear indication that many Americans are feeling anxious. Addressing this anxiety requires not only sound economic policy but also reassurance and a clear vision for how the nation plans to navigate the current economic challenges.

Conclusion: A Critical Juncture for the U.S. Economy

The recent three-month dip in U.S. consumer confidence is a significant development that demands careful attention. It reflects a growing sense of unease among American households, primarily driven by persistent inflation, rising borrowing costs, and broader economic uncertainties. This decline in sentiment has direct implications for consumer spending, business investment, and overall economic growth.

While the U.S. economy has shown resilience in many areas, the sustained consumer confidence dip suggests that the cumulative effect of these pressures is taking its toll. Understanding these dynamics is crucial for individuals making financial decisions, for businesses strategizing their next moves, and for policymakers charting the course for the nation’s economic future.

The path forward will likely involve a continued balancing act, with careful monitoring of inflation, employment figures, and global developments. A return to robust consumer confidence will depend on a combination of factors: a sustained cooling of inflation, stability in interest rates, and a clearer, more positive outlook on job security and economic growth. Until then, the recent dip serves as a potent reminder of the interconnectedness of economic indicators and the profound impact of consumer sentiment on the health of the entire economy.