HSA vs. FSA 2026: Unlocking Maximum Tax Benefits for Healthcare

Anúncios

HSA vs. FSA 2026: Unlocking Maximum Tax Benefits for Healthcare

In the ever-evolving landscape of healthcare financing, understanding your options for managing medical expenses is paramount. As we look ahead to 2026, two primary contenders for tax-advantaged healthcare savings continue to dominate the discussion: Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). Both offer significant benefits, but their structures, eligibility requirements, and long-term implications differ dramatically. Deciding between an HSA and an FSA, or understanding how they might complement each other, can be a complex endeavor, yet it’s a decision that profoundly impacts your financial well-being and healthcare accessibility.

Anúncios

The goal of this comprehensive guide is to meticulously compare HSA FSA 2026, dissecting their unique features, tax advantages, and limitations. We aim to equip you with the knowledge necessary to make an informed decision that aligns with your individual health needs, financial goals, and risk tolerance. Whether you’re a seasoned professional navigating open enrollment or a newcomer to the intricacies of healthcare savings, this article will serve as your definitive resource for understanding which account offers better tax benefits and overall utility in the coming years.

Navigating the healthcare system can be daunting, but optimizing your healthcare spending doesn’t have to be. With the right strategy, you can leverage these powerful tools to reduce your taxable income, save for future medical costs, and gain greater control over your health finances. Let’s dive deep into the world of HSA FSA 2026 and uncover the strategies that can lead to significant savings.

Anúncios

Understanding the Fundamentals: What Are HSAs and FSAs?

Before we delve into a detailed comparison of HSA FSA 2026, it’s crucial to establish a clear understanding of what each account entails. While both are designed to help individuals save for and pay for qualified medical expenses with pre-tax dollars, their underlying mechanics and long-term implications are quite distinct.

Health Savings Accounts (HSAs): The Long-Term Investment Vehicle

An HSA is a tax-advantaged savings account that can be used for healthcare expenses. Critically, to be eligible for an HSA, you must be enrolled in a High-Deductible Health Plan (HDHP) and not be enrolled in Medicare, nor be claimed as a dependent on someone else’s tax return. This prerequisite is fundamental to understanding the HSA’s design and purpose. HDHPs typically have lower monthly premiums but higher deductibles, meaning you pay more out-of-pocket before your insurance kicks in. The HSA is designed to help you cover these higher initial costs.

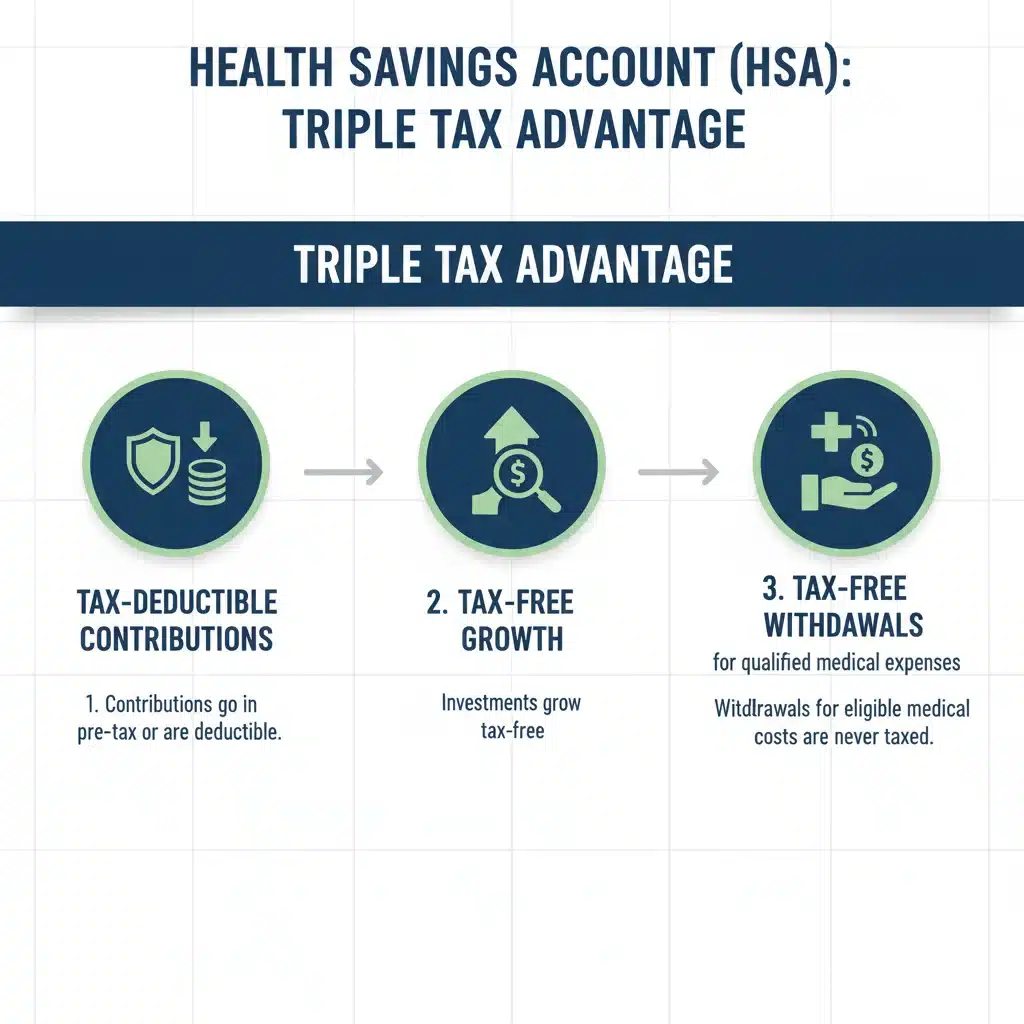

The defining characteristic of an HSA is its ‘triple tax advantage’:

- Tax-Deductible Contributions: Money you contribute to an HSA is tax-deductible, reducing your taxable income for the year.

- Tax-Free Growth: The funds in an HSA can be invested, and any earnings (interest, dividends, capital gains) grow tax-free. This is a significant advantage, effectively making an HSA a powerful retirement savings vehicle for healthcare.

- Tax-Free Withdrawals: When you withdraw funds for qualified medical expenses, those withdrawals are completely tax-free.

Unlike FSAs, HSAs are portable and belong to you, not your employer. The funds roll over year after year, never expiring, and can even be used in retirement for non-medical expenses (though they would then be subject to income tax, similar to a traditional IRA). This makes the HSA a unique blend of a healthcare savings account and a long-term investment tool, particularly appealing to those looking for a robust HSA FSA 2026 strategy.

Flexible Spending Accounts (FSAs): The Annual Healthcare Budget

An FSA, on the other hand, is an employer-sponsored benefit that allows you to set aside pre-tax money from your paycheck to pay for eligible out-of-pocket healthcare costs. Unlike HSAs, you do not need to be enrolled in an HDHP to participate in an FSA. Most individuals with employer-provided health insurance are eligible.

The primary tax advantage of an FSA is that contributions are made with pre-tax dollars, reducing your taxable income. However, the most significant distinction from an HSA is the ‘use-it-or-lose-it’ rule. Generally, FSA funds must be used within the plan year or a short grace period (typically 2.5 months) immediately following the plan year, or they are forfeited. Some employers may allow a limited amount to roll over to the next year, but this is an exception rather than the rule.

FSAs are ideal for individuals who anticipate consistent, predictable healthcare expenses each year, such as co-pays, deductibles, prescriptions, and certain over-the-counter items. They offer immediate tax savings on those anticipated expenses. When considering HSA FSA 2026, the ‘use-it-or-lose-it’ aspect is a critical factor that differentiates it significantly from an HSA.

HSA vs. FSA 2026: A Detailed Comparison of Key Features

Now that we have a foundational understanding of both accounts, let’s conduct a direct comparison of HSA FSA 2026 across several key dimensions, focusing on eligibility, contribution limits, portability, investment potential, and withdrawal rules.

Eligibility Requirements

- HSA: Strict eligibility. Must be covered by an HDHP, not enrolled in Medicare, and not claimed as a dependent. This linkage to HDHPs is a cornerstone of HSA eligibility.

- FSA: More broadly accessible. Available through an employer, regardless of your health plan type. You cannot have both an HSA and a general-purpose FSA simultaneously, though a Limited Purpose FSA (for dental/vision) can be combined with an HSA.

Contribution Limits for 2026 (Projected)

Contribution limits are adjusted annually for inflation. While official 2026 limits are not yet released, we can project based on past trends. For 2025, the limits were $4,300 for self-only coverage and $8,550 for family coverage, with an additional $1,000 catch-up contribution for those aged 55 and over. We can anticipate a slight increase for 2026. These limits are crucial for maximizing your HSA FSA 2026 tax benefits.

- HSA: Higher contribution limits compared to FSAs, allowing for more substantial tax-deductible savings. These limits are set by the IRS.

- FSA: Generally lower contribution limits, typically around $3,200 for 2024, with slight increases expected for 2025 and 2026. These limits are also set by the IRS.

Portability and Rollover Rules

- HSA: Fully portable. The account belongs to you, not your employer. Funds roll over year after year indefinitely. You can take it with you if you change jobs or health plans. This is a massive advantage for long-term financial planning.

- FSA: Generally not portable. Tied to your employer. Funds typically expire at the end of the plan year (‘use it or lose it’). Some employers offer a grace period or a limited rollover (e.g., up to $640 for 2024, likely to increase slightly for 2026), but this is not universal.

Investment Potential

- HSA: Can be invested in a wide range of options, similar to an IRA or 401(k), once a certain threshold balance is met. This allows for significant tax-free growth over time, making it a powerful retirement savings tool. This investment aspect is a key differentiator when evaluating HSA FSA 2026.

- FSA: Funds cannot be invested. They are held in a standard account and are only used for immediate healthcare expenses.

Withdrawal Rules and Penalties

- HSA: Tax-free withdrawals for qualified medical expenses at any age. After age 65 (or if you become disabled), withdrawals for non-medical expenses are treated like traditional IRA withdrawals – subject to income tax but no penalty. Before age 65, non-medical withdrawals are subject to income tax and a 20% penalty.

- FSA: Tax-free withdrawals for qualified medical expenses only. Withdrawals for non-medical expenses are not permitted.

Tax Benefits Deep Dive: HSA vs. FSA 2026

The core appeal of both HSAs and FSAs lies in their tax advantages. However, the nature and extent of these benefits differ significantly. Understanding these nuances is key to determining which account offers superior tax benefits for your specific situation in 2026.

HSA: The Triple Tax Advantage Explained

As mentioned, the HSA boasts a ‘triple tax advantage’ that makes it a uniquely powerful financial tool:

- Tax-Deductible Contributions: Contributions made by you are deductible on your federal income taxes, even if you don’t itemize. If your employer contributes, those contributions are excluded from your gross income. This immediate tax reduction can be substantial.

- Tax-Free Growth: This is where the HSA truly shines as an investment vehicle. Any interest, dividends, or capital gains earned on the invested funds within your HSA are completely tax-free. Over decades, this tax-free compounding can lead to significant wealth accumulation. For instance, if you contribute regularly and invest wisely, your HSA could grow into a substantial sum, providing a tax-free reservoir for future medical needs in retirement.

- Tax-Free Withdrawals for Medical Expenses: When you use HSA funds for qualified medical expenses, the withdrawals are entirely tax-free. This means you avoid taxes on the money going in, the money growing, and the money coming out for healthcare. This makes HSA FSA 2026 comparisons heavily lean towards HSAs for long-term tax efficiency.

Furthermore, after age 65, HSA funds can be withdrawn for any purpose without penalty. While non-medical withdrawals are subject to ordinary income tax (like a traditional IRA or 401(k)), the ability to use these funds for general retirement expenses adds another layer of flexibility and tax planning opportunity.

FSA: Immediate Tax Savings on Predictable Expenses

The tax benefit of an FSA is more straightforward:

- Pre-Tax Contributions: Money is deducted from your paycheck before taxes are calculated, reducing your taxable income. This means you save on federal income tax, Social Security, and Medicare taxes.

- Tax-Free Withdrawals for Medical Expenses: Funds withdrawn for qualified medical expenses are tax-free.

While an FSA offers immediate tax savings, it lacks the investment growth potential and the long-term portability of an HSA. Its primary role is to provide a current-year tax break on anticipated medical spending. For individuals with consistent medical needs, an FSA can be an excellent way to reduce the effective cost of those expenses.

Which Offers Better Tax Benefits: HSA FSA 2026?

From a purely tax-advantaged perspective, the HSA generally comes out on top due to its ‘triple tax advantage’ and its ability to function as a long-term investment vehicle. The tax-free growth and the flexibility to use funds in retirement for non-medical expenses (after age 65) provide a significant edge. For those who can afford to pay for current medical expenses out-of-pocket and let their HSA funds grow, the tax benefits are unparalleled.

However, the FSA offers immediate and guaranteed tax savings for those who have predictable medical expenses and might not be eligible for an HDHP, or prefer a traditional health plan. It’s a ‘sure thing’ for current year savings, whereas the HSA’s full benefits are often realized over a longer horizon through investment growth. The choice between HSA FSA 2026 ultimately depends on your health plan, financial situation, and spending habits.

Navigating Eligibility and Contribution Limits for 2026

Understanding the precise rules for eligibility and contribution limits is fundamental to effectively utilizing either an HSA or an FSA in 2026. These parameters dictate who can participate and how much they can contribute, directly influencing the potential tax benefits.

HSA Eligibility in 2026

The core requirement for an HSA remains enrollment in a High-Deductible Health Plan (HDHP). For 2025, an HDHP is defined as a plan with a minimum deductible of $1,650 for self-only coverage and $3,300 for family coverage. The maximum out-of-pocket expenses (including deductibles, co-payments, and co-insurance) cannot exceed $8,300 for self-only coverage and $16,600 for family coverage. These figures are expected to see a slight increase for 2026 due to inflation adjustments by the IRS. It’s crucial to verify the exact 2026 HDHP thresholds when they are released.

Beyond the HDHP requirement, you must not be:

- Enrolled in Medicare.

- Claimed as a dependent on someone else’s tax return.

- Covered by any other non-HDHP health insurance (with some exceptions for specific vision, dental, or accident insurance).

This strict eligibility criteria means that not everyone can benefit from an HSA, making the HSA FSA 2026 decision often pre-determined by your health insurance choice.

FSA Eligibility in 2026

FSA eligibility is simpler: you must be employed by a company that offers an FSA benefit. You do not need a specific type of health plan, and unlike HSAs, FSAs are generally available to anyone whose employer offers them. However, it’s important to note that you cannot typically have both a general-purpose FSA and an HSA at the same time. If you have an HDHP and want an HSA, your employer might offer a ‘Limited Purpose FSA’ which can only be used for dental and vision expenses, allowing you to contribute to both.

Projected Contribution Limits for HSA FSA 2026

While the official 2026 limits will be released later, we can anticipate them based on the 2025 figures. For 2025, HSA contribution limits were:

- Self-only coverage: $4,300

- Family coverage: $8,550

- Catch-up contribution (age 55+): Additional $1,000

These limits are indexed for inflation, so expect a modest increase for 2026. Maximizing these contributions is key to leveraging the tax benefits of an HSA. The higher the contribution, the greater the immediate tax deduction and the more funds available for tax-free growth.

For FSAs, the 2024 contribution limit was $3,200. This limit is also subject to annual inflation adjustments. For 2025 and 2026, we can expect a slight increase, likely in the range of $50-$100 per year. While lower than HSA limits, the FSA still offers valuable tax savings on anticipated medical expenses.

It’s crucial to stay updated on the official IRS announcements for 2026 contribution limits to ensure you’re maximizing your savings and remaining compliant. Planning your contributions carefully, especially for an FSA, is vital to avoid the ‘use-it-or-lose-it’ scenario.

Strategic Considerations: When to Choose Which Account

The choice between an HSA and an FSA is not always straightforward and often depends on your personal circumstances, health status, and financial outlook. Here’s a strategic breakdown to help you decide for HSA FSA 2026.

When an HSA (Health Savings Account) is the Better Choice:

- You are enrolled in an HDHP: This is the fundamental requirement. If you choose an HDHP, an HSA becomes a viable and often superior option.

- You are healthy and have low, predictable medical expenses: If you don’t anticipate hitting your high deductible regularly, you can let your HSA funds grow through investments, building a significant nest egg for future healthcare needs, especially in retirement.

- You want a long-term investment vehicle: The ability to invest HSA funds and benefit from tax-free growth makes it an excellent addition to your retirement portfolio. It’s often referred to as the ‘triple tax-advantaged’ account.

- You want portability: HSA funds are yours to keep, even if you change jobs or retire. They never expire.

- You can afford to pay for current medical expenses out-of-pocket: This allows your HSA balance to grow untouched, maximizing its investment potential. You can reimburse yourself later for qualified expenses, even years down the line, as long as you keep meticulous records.

- You are planning for retirement healthcare costs: Healthcare costs in retirement can be substantial. An HSA provides a dedicated, tax-advantaged fund to cover these expenses.

When an FSA (Flexible Spending Account) is the Better Choice:

- You are not eligible for an HSA: If you don’t have an HDHP, an FSA is likely your best option for pre-tax healthcare savings.

- You have consistent, predictable medical expenses each year: If you know you’ll incur a certain amount in co-pays, prescriptions, or other eligible expenses, an FSA allows you to pay for these with pre-tax dollars, saving you money immediately.

- You prefer immediate tax savings over long-term investment growth: While HSAs offer investment potential, FSAs provide immediate tax relief on current healthcare costs.

- You are comfortable with the ‘use-it-or-lose-it’ rule: You must be diligent in spending your FSA funds within the plan year (or grace period) to avoid forfeiture. This requires careful planning.

- Your employer offers a generous FSA contribution: Some employers contribute to FSAs, which adds to the benefit.

Can You Have Both an HSA and an FSA in 2026?

Generally, no, you cannot have both a general-purpose FSA and an HSA simultaneously, as the FSA would disqualify you from HSA eligibility. However, there’s a crucial exception: a Limited-Purpose FSA (LPFSA). An LPFSA is restricted to covering only dental and vision expenses. If you have an HDHP and an HSA, your employer might offer an LPFSA, allowing you to use pre-tax funds for those specific expenses while still contributing to and growing your HSA for broader medical costs. This can be an excellent strategy for maximizing HSA FSA 2026 benefits.

Maximizing Your Healthcare Savings: Best Practices for 2026

Regardless of whether you choose an HSA, an FSA, or a combination (with an LPFSA), adopting best practices can significantly enhance your healthcare savings and overall financial health in 2026.

For HSA Holders:

- Maximize Contributions: Aim to contribute the full annual limit whenever possible. The more you put in, the greater your tax deduction and the more funds you have to grow tax-free.

- Invest Your Funds: Don’t just let your HSA sit in cash. Explore the investment options offered by your HSA administrator. Even conservative investments can yield significant returns over time, leveraging the triple tax advantage.

- Pay Out-of-Pocket (If Possible): If you have the financial capacity, pay for current medical expenses with after-tax dollars and let your HSA funds continue to grow. You can keep records of these expenses and reimburse yourself tax-free from your HSA at any point in the future, even decades later. This is a powerful strategy for maximizing long-term growth.

- Keep Meticulous Records: If you plan to pay out-of-pocket and reimburse yourself later, keep all receipts and Explanation of Benefits (EOB) statements for qualified medical expenses. This is vital for tax-free withdrawals in the future.

- Understand Qualified Medical Expenses: Familiarize yourself with what constitutes a qualified medical expense according to IRS Publication 502. This ensures your withdrawals are tax-free.

For FSA Holders:

- Estimate Expenses Carefully: Due to the ‘use-it-or-lose-it’ rule, it’s crucial to accurately estimate your anticipated medical expenses for the year. Over-contributing can lead to forfeiture of funds.

- Plan Your Spending: Keep track of your FSA balance and plan to use it before the deadline. Don’t wait until the last minute. Consider scheduling elective procedures or purchasing eligible over-the-counter items towards the end of the year if you have remaining funds.

- Know Your Employer’s Rules: Understand if your employer offers a grace period or a limited rollover for FSA funds. This can provide a small buffer.

- Utilize Your FSA Debit Card: Many FSAs come with a debit card, making it easy to pay for eligible expenses directly and track your spending.

- Review Eligible Expenses: The list of eligible FSA expenses is extensive and can include prescriptions, co-pays, deductibles, dental care, vision care, and even some over-the-counter medications and menstrual products. Refer to IRS Publication 502 or your plan administrator’s list for details.

General Tips for Both:

- Stay Informed: Tax laws and contribution limits can change annually. Keep an eye on IRS announcements for 2026 to ensure you’re up-to-date.

- Review Annually: Each open enrollment period is an opportunity to re-evaluate your health plan and healthcare savings strategy. Your health needs and financial situation can change, so what worked last year might not be optimal for HSA FSA 2026.

- Consult a Financial Advisor: For complex financial situations or significant healthcare planning, a qualified financial advisor can provide personalized guidance.

The Future of Healthcare Savings: Trends for HSA FSA 2026 and Beyond

As we move towards 2026 and beyond, the landscape of healthcare savings accounts continues to evolve. Several trends are shaping how individuals and employers approach HSAs and FSAs.

Increasing Popularity of HDHPs and HSAs

The trend towards High-Deductible Health Plans (HDHPs) has been steadily growing, largely driven by employers seeking to control healthcare costs. As HDHPs become more common, so too does the eligibility and adoption of HSAs. This trend is likely to continue, making HSAs an increasingly central component of many Americans’ financial planning. The long-term investment potential of HSAs, especially for younger generations, is becoming more widely recognized, leading to greater emphasis on maximizing contributions and investing the funds.

Focus on Financial Wellness and Education

Employers and financial institutions are placing a greater emphasis on financial wellness programs, which often include education on HSAs and FSAs. As healthcare costs continue to rise, empowering individuals to make informed decisions about their healthcare savings is critical. Expect more resources and tools designed to help people understand the nuances of HSA FSA 2026 and how to optimize their benefits.

Technological Advancements and Integration

Digital platforms for managing HSAs and FSAs are becoming more sophisticated, offering easier tracking of expenses, investment options, and integration with other financial tools. Mobile apps, AI-powered expense categorization, and seamless payment solutions will likely enhance the user experience and simplify the management of these accounts, making it easier to leverage the benefits of HSA FSA 2026.

Potential for Policy Changes

While the fundamental structures of HSAs and FSAs are well-established, there’s always the potential for legislative changes that could impact contribution limits, eligible expenses, or other rules. Staying informed about potential policy shifts is important for long-term planning. However, the core tax advantages of HSAs and FSAs are deeply embedded in the tax code and are expected to remain robust.

The Role of Limited-Purpose FSAs

For those with HSAs, the Limited-Purpose FSA (LPFSA) is gaining traction as a way to cover immediate dental and vision costs with pre-tax dollars, allowing the primary HSA to grow untouched for larger medical expenses or retirement. This strategic combination of HSA FSA 2026 tools offers an optimized approach for many individuals.

Conclusion: Making Your Informed Decision for HSA FSA 2026

Choosing between an HSA and an FSA for 2026, or understanding how to best utilize them, is a critical component of effective financial and healthcare planning. Both offer valuable tax advantages, but their suitability depends entirely on your individual circumstances.

The Health Savings Account (HSA) stands out for its ‘triple tax advantage’ – tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses – coupled with its portability and investment potential. It’s an ideal choice for individuals enrolled in a High-Deductible Health Plan who seek a long-term savings and investment vehicle for current and future healthcare costs, especially those looking ahead to retirement.

The Flexible Spending Account (FSA), while lacking the investment component and long-term portability of an HSA, offers immediate tax savings on predictable, current-year medical expenses. It’s an excellent option for those not eligible for an HSA or who prefer a traditional health plan and have a clear understanding of their annual healthcare spending.

As you plan for HSA FSA 2026, take the time to:

- Assess your health plan eligibility: Are you in an HDHP?

- Evaluate your anticipated medical expenses: Are they predictable and consistent, or are you generally healthy with few current needs?

- Consider your long-term financial goals: Do you want an investment vehicle for retirement healthcare, or primarily a way to save on current taxes?

- Understand the ‘use-it-or-lose-it’ rule for FSAs: Are you comfortable with careful planning to avoid forfeiture?

By carefully weighing these factors and staying informed about the latest IRS regulations and contribution limits, you can confidently choose the healthcare savings account (or combination) that best aligns with your needs, helping you unlock maximum tax benefits and secure your financial future in 2026 and beyond.