Optimizing Investment for Inflation in 2026: 7% Hedging

Anúncios

To optimize your investment strategy against 2026 inflation, a proactive 7% hedging approach is crucial for safeguarding your portfolio’s real value amidst economic uncertainties and market volatility.

Anúncios

As we look towards 2026, the economic landscape continues to evolve, making the need for an effective optimizing investment strategy more critical than ever, especially concerning inflation. Understanding how to protect your portfolio with a robust hedging approach isn’t just prudent; it’s essential for preserving and growing your wealth in an environment where purchasing power can erode rapidly.

Anúncios

Understanding the Inflationary Landscape in 2026

The year 2026 presents a unique set of challenges and opportunities for investors. While central banks strive for price stability, various global and domestic factors can contribute to persistent inflationary pressures. Understanding these nuances is the first step in formulating a resilient investment strategy.

Economic forecasts for 2026 suggest that while some inflationary pressures might subside, others could emerge or intensify. Supply chain disruptions, geopolitical tensions, and shifts in consumer spending habits are just a few elements that could fuel price increases. Investors must therefore remain vigilant and adaptable.

Key Drivers of Inflation in 2026

- Global Supply Chain Resilience: Ongoing efforts to diversify supply chains might lead to higher production costs initially, feeding into consumer prices.

- Labor Market Dynamics: Persistent wage growth pressures in tight labor markets can contribute to cost-push inflation.

- Commodity Price Volatility: Energy and food prices, influenced by geopolitical events and climate change, can significantly impact overall inflation rates.

- Fiscal and Monetary Policies: Government spending and central bank interest rate decisions will play a pivotal role in shaping the inflationary environment.

Navigating this complex environment requires not only an understanding of the past but also a forward-looking perspective. Investors who can anticipate potential inflationary triggers and adjust their portfolios accordingly will be better positioned to mitigate risks and capitalize on opportunities. This proactive stance is fundamental to an optimized investment strategy.

The Importance of a 7% Hedging Approach

A 7% hedging approach isn’t an arbitrary figure; it represents a strategic target for mitigating the impact of inflation on your portfolio’s real returns. This level of hedging aims to offset a significant portion of potential purchasing power erosion, ensuring your investments maintain their value over time. It’s about being conservative enough to protect, yet aggressive enough to grow.

Implementing a 7% hedge means consciously allocating a portion of your portfolio to assets historically known to perform well during inflationary periods. This isn’t about predicting exact inflation rates, but rather building a robust defense against various potential scenarios. The objective is to create a buffer that sustains your capital’s buying power.

Why 7%? Balancing Risk and Reward

The 7% target strikes a balance between over-hedging, which can lead to missed growth opportunities in non-inflationary periods, and under-hedging, which leaves your portfolio vulnerable. It acknowledges that moderate-to-high inflation can be a persistent challenge, requiring a dedicated protective measure without stifling overall portfolio growth.

- Historical Performance: Analyzing past inflationary cycles reveals that certain asset classes consistently outperform when inflation is elevated.

- Diversification Benefits: A targeted hedging allocation enhances overall portfolio diversification, reducing correlation risk during economic shifts.

- Real Return Preservation: The primary goal is to preserve the real (inflation-adjusted) return of your investments, ensuring your wealth doesn’t diminish in value.

Achieving this 7% hedge requires careful selection of assets and a disciplined rebalancing strategy. It’s not a one-time adjustment but an ongoing process that adapts to changing market conditions. This focused approach provides a clear framework for investors seeking to fortify their financial positions against future price increases.

Diversifying for Inflation Resilience

Diversification is the cornerstone of any sound investment strategy, and it becomes even more critical when facing inflationary pressures. A diversified portfolio, specifically structured for inflation resilience, spreads risk across various asset classes that tend to behave differently during periods of rising prices. This reduces the impact of any single asset’s underperformance.

Beyond traditional stocks and bonds, smart diversification for inflation involves looking at assets with a strong historical correlation to inflation. These can include real assets, certain types of equities, and specialized financial instruments designed to offer protection. The goal is to build a portfolio that can weather market storms and maintain its intrinsic value.

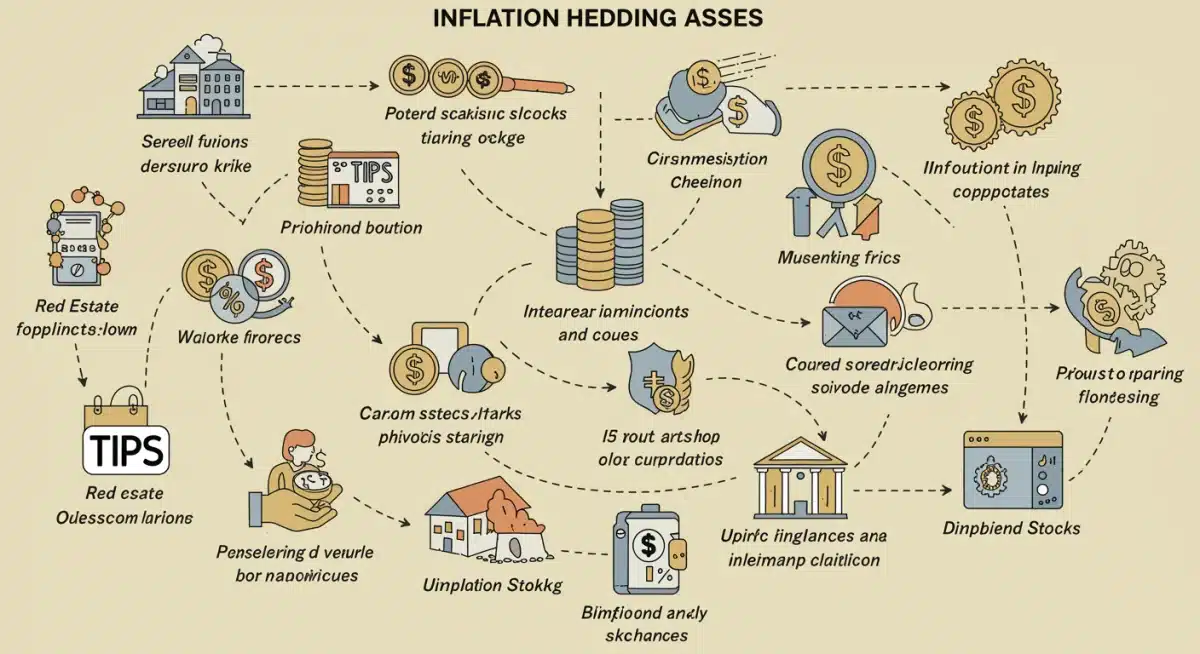

Key Asset Classes for Inflation Hedging

To effectively diversify for inflation, consider these asset categories:

- Real Estate: Historically, real estate, particularly income-generating properties, has acted as a strong hedge against inflation. Rents and property values often rise with the cost of living.

- Commodities: Raw materials like gold, silver, oil, and agricultural products tend to appreciate when inflation is high, as their prices are directly tied to the cost of goods.

- Treasury Inflation-Protected Securities (TIPS): These government bonds are specifically designed to protect against inflation, with their principal value adjusting to changes in the Consumer Price Index (CPI).

- Dividend-Paying Stocks: Companies with strong pricing power and consistent dividend growth can offer a degree of inflation protection, as their earnings and payouts may increase over time.

- Infrastructure Investments: Assets such as toll roads, utilities, and energy pipelines often have inflation-linked revenue streams, providing a steady income that adjusts with rising prices.

Building a diversified portfolio for inflation resilience requires a thoughtful allocation strategy. It’s about finding the right mix of these assets that aligns with your risk tolerance and long-term financial goals, ensuring your portfolio is robust against various economic scenarios.

Strategic Allocation and Rebalancing for the 7% Hedge

Achieving the 7% hedging target isn’t just about selecting the right assets; it’s also about strategic allocation and diligent rebalancing. Initial allocation sets the foundation, but market dynamics necessitate regular adjustments to maintain the desired hedge level and ensure optimal performance. This active management is crucial for long-term success.

A well-defined allocation strategy considers your overall portfolio size, risk appetite, and investment horizon. The 7% hedge should be integrated into your broader asset allocation framework, rather than being treated as a separate, isolated component. It’s a continuous process of evaluation and adjustment to market realities.

Implementing Your Allocation Strategy

When allocating for your 7% hedge, consider these steps:

- Assess Current Portfolio Exposure: Understand how much of your existing portfolio is already exposed to inflation-sensitive assets.

- Identify Gaps: Determine which asset classes are underrepresented in your current inflation hedging strategy.

- Allocate Incrementally: Gradually build up your hedging positions, rather than making drastic, sudden changes, to average out entry points.

The Role of Rebalancing

Rebalancing is vital to maintain your 7% hedging target. As market values fluctuate, the percentage allocation of your hedging assets will drift. Regular rebalancing brings your portfolio back to its target weights, ensuring your protective measures remain effective.

- Periodic Reviews: Schedule quarterly or semi-annual reviews to assess your portfolio’s asset allocation.

- Adjust as Needed: Sell assets that have performed strongly (and now exceed their target allocation) and buy those that have underperformed (and are below target) to restore balance.

- Stay Disciplined: Avoid emotional decisions during rebalancing; stick to your predetermined strategy.

Strategic allocation and consistent rebalancing are the twin pillars of maintaining an effective 7% inflation hedge. They ensure your portfolio remains aligned with your protective goals, adapting to market shifts without compromising your long-term objectives.

Leveraging Alternative Investments and Specialized Funds

Beyond traditional asset classes, alternative investments and specialized funds offer unique avenues for enhancing your inflation hedging strategy. These options can provide diversification benefits and exposure to assets that might be less correlated with conventional markets, offering additional layers of protection during inflationary periods.

Exploring alternatives requires a deeper understanding of their underlying mechanisms and associated risks. However, for sophisticated investors, they can be powerful tools to achieve the targeted 7% hedge and potentially generate superior risk-adjusted returns. It’s about looking beyond the obvious to find tailored solutions.

Exploring Niche Inflation Hedges

Consider these alternative and specialized approaches:

- Infrastructure Funds: Investments in private or publicly traded infrastructure funds can provide exposure to assets with predictable, often inflation-linked, cash flows.

- Private Equity/Debt with Inflation Clauses: Some private market investments may include clauses that adjust returns based on inflation, offering direct protection.

- Managed Futures: These strategies can profit from trends in commodity markets, currencies, and interest rates, which often correlate with inflationary cycles.

- Real Asset Funds: Funds that invest directly in a basket of real assets, such as timberland, farmland, or natural resources, can provide broad inflation exposure.

While these options can offer significant benefits, they often come with higher fees, liquidity constraints, and increased complexity. Thorough due diligence and consultation with a financial advisor are essential before incorporating them into your portfolio. The goal is to enhance your hedge without introducing undue risk.

Leveraging alternative investments and specialized funds can be a sophisticated way to bolster your 7% inflation hedging strategy. They provide additional tools to diversify and protect your portfolio, offering exposure to unique market segments that thrive in inflationary environments.

Monitoring and Adapting Your Strategy Post-2026

An effective investment strategy is never static; it requires continuous monitoring and adaptation. While we focus on 2026, the economic landscape will continue to evolve, necessitating vigilance beyond that horizon. Regularly reviewing your portfolio’s performance against inflation and making necessary adjustments is paramount for long-term financial health.

The 7% hedging approach is a dynamic target, not a fixed endpoint. As economic conditions change, so too might the optimal level of hedging or the most effective assets for achieving it. Your strategy should be flexible enough to respond to new data and emerging trends.

Key Monitoring Practices

To ensure your strategy remains effective:

- Track Inflation Indicators: Keep an eye on various inflation metrics, not just the CPI, to get a comprehensive view of price pressures.

- Review Portfolio Performance: Regularly assess how your hedging assets are performing relative to your overall portfolio and inflation rates.

- Stay Informed: Follow economic news, central bank announcements, and geopolitical developments that could impact inflation.

Adapting to New Realities

- Adjusting Hedging Percentage: If inflation trends significantly higher or lower than anticipated, you might need to adjust your 7% target.

- Refining Asset Allocation: As certain assets become more or less effective as inflation hedges, reallocate capital to maintain optimal protection.

- Exploring New Instruments: Be open to incorporating new financial products or strategies that emerge as effective inflation fighters.

Monitoring and adapting your investment strategy are ongoing processes that ensure your portfolio remains resilient against inflation well beyond 2026. This proactive and flexible approach is the hallmark of a truly optimized investment strategy, safeguarding your wealth for the future.

| Key Point | Brief Description |

|---|---|

| 7% Hedging Goal | A strategic target to protect portfolio real value against inflation. |

| Diversification | Spread risk across real estate, commodities, TIPS, and dividend stocks. |

| Rebalancing | Regular adjustments to maintain target asset allocations and hedging levels. |

| Alternative Investments | Consider infrastructure funds or managed futures for enhanced protection. |

Frequently Asked Questions About Inflation Hedging

Inflation hedging involves investing in assets expected to retain or increase their value during periods of rising prices. The goal is to protect the purchasing power of your investment portfolio and ensure your wealth isn’t eroded by inflation.

A 7% hedging approach is a strategic target that balances adequate protection against potential inflation in 2026 with opportunities for growth. It aims to create a robust defense without excessively limiting your portfolio’s overall return potential.

Key assets for inflation hedging include real estate, commodities (like gold and oil), Treasury Inflation-Protected Securities (TIPS), dividend-paying stocks, and certain infrastructure investments. Diversifying across these can offer broad protection.

Regular rebalancing is crucial, typically quarterly or semi-annually. This ensures your portfolio maintains its target asset allocation and the desired 7% hedging level, adapting to market fluctuations and keeping your strategy effective.

Yes, alternative investments like infrastructure funds, private equity with inflation clauses, and managed futures can enhance your inflation hedging strategy. They offer unique diversification benefits and exposure to assets that are less correlated with traditional markets.

Conclusion

As we navigate towards and beyond 2026, the imperative to optimize your investment strategy for inflation cannot be overstated. Implementing a disciplined 7% hedging approach, diversified across resilient asset classes and actively managed through rebalancing, offers a robust framework for protecting your portfolio’s real value. Staying informed and adaptable will be key to preserving and growing your wealth in an ever-changing economic landscape.

s: Alternative Investments for 2026")